The explosive growth in artificial intelligence (AI) data workloads is straining the physical limits of data centers. As generative AI models expand in size, training clusters demand ever-higher bandwidths. As a result, these systems are testing the physical thresholds for traditional copper interconnects on speed, power consumption, and heat.

Optical interconnects, which use pulses of light instead of electrons to transmit data, promise to enable faster, cooler, and more efficient communication between chips and servers.

Industry research suggests the optical AI accelerator market could grow from about $2 billion this year to $146 billion by 2040, driven by rising demand from hyperscalers for energy-efficient photonics in high-performance computing.

In this landscape, Poet Technologies (POET 11.02%) has emerged as a potential disruptor thanks to its proprietary Optical Interposer platform. Yet despite the massive opportunity, a closer look at the company's fundamentals reveals why it is not a compelling buy right now.

Poet's Optical Interposer is a silicon-based platform that integrates photonic components directly with electronic circuits. This wafer-level architecture eliminates costly and error-prone alignment steps seen in conventional optical modules.

By bringing optics closer to compute links, Poet hopes to meaningfully reduce both latency and power consumption while simultaneously scaling bandwidth to meet big tech's growing appetite for GPU clusters. The company is co-developing its optical modules with Taiwan-based Lite-On Technology, with prototypes scheduled for late 2026 and high-volume production targeted for 2027.

Most recently, Lumilens signed $50 million purchase order for Poet's Electrical-Optical Interposer engines aimed at frontier AI infrastructure, under a joint development agreement. The deal is structured to support cumulative purchases that could exceed $500 million over five years.

Image source: The Motley Fool.

For all its technical aspirations, Poet has thus far generated little buzz within broader AI conversations, which are dominated by chip designers, hyperscalers, and enterprise software developers. In my opinion, that lack of chatter is due to the fact that Poet is still at a fairly early stage of its development: The company is still transitioning from capital-intensive research and development to meaningful commercial sales. The spotlight in photonics, which is itself limited at the moment, is reserved for larger incumbents.

For example, with its dominant role in designing high-speed networking application-specific integrated circuits (ASICs), Broadcom has leveraged its prowess to build an entrenched position in optical modules through a savvy vertical integration strategy at a massive scale.

Cisco is also bringing deep silicon photonics expertise to its hyperscaler relationships thanks to its 2021 acquisition of Acacia Communications. In addition, Marvell Technology is a market leader in high-speed digital signal processors and optical engines that can easily be bundled with broader networking solutions. Lastly, laser specialists like Coherent and Lumentum have received a combined $4 billion in strategic investments from Nvidia — likely in recognition of their manufacturing scale and established supply chains.

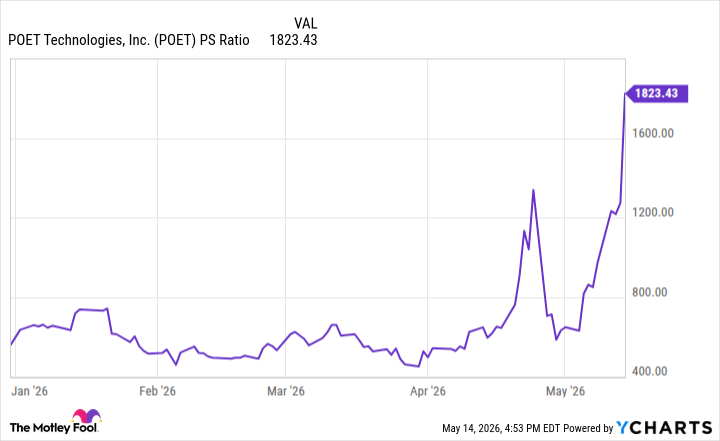

Despite an exciting narrative, Poet stock is not a buy now when viewed through the lens of its size, valuation, and total addressable market. The company's market capitalization of $2.7 billion is overstretched for a business that generated just $1.1 million in sales over the past year.

POET PS Ratio data by YCharts.

While the optical interconnect market has genuine secular tailwinds driven by the power and latency bottlenecks that AI data centers are facing, Poet's current footprint positions it to capture only the tiniest sliver of the overall opportunity. Notably, its deal with Lumilens does little to change this. Yet investors have already bid up the stock to a level that assumes that Poet will both secure and defend a sizable chunk of this exploding pocket of the AI infrastructure realm.

Poet's valuation has soared far above any realistic near-term trajectory or proven execution. Buying at its current price leaves no margin of safety if commercialization slips or if the tech sector players who are expected to adopt photonic interconnects tend to favor larger, better-capitalized incumbents. Until Poet's valuation realigns with its actual business, the company will be more of a fascinating watch list name rather than a durable, investable opportunity.

Adam Spatacco has positions in Nvidia. The Motley Fool has positions in and recommends Broadcom, Cisco Systems, Coherent, Lumentum, Marvell Technology, and Nvidia. The Motley Fool has a disclosure policy.

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.

Making the world smarter, happier, and richer.

© 1995 – 2026 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.

About The Motley Fool

Our Services

Around the Globe

Free Tools

Affiliates & Friends

Poet Technologies is gaining steam in the artificial intelligence (AI) infrastructure market, but its stock has gotten well ahead of its business.

This Artificial Intelligence (AI) Semiconductor Company Has a $146 Billion Opportunity That No One Is Talking About. Here's Why the Stock Still Isn't a Buy. – The Motley Fool

Leave a Comment